How Credit Scores Quietly Shape a Life

By Vicky Tang

https://www.experian.com/blogs/ask-experian/credit-education/score-basics/what-is-a-good-credit-score/

1.Why Credit Scores Matter More Than You Think

Most of people are raised to think of the credit score in much the same way we think of a simple tool: you take a quick look at it when applying for a credit card, a lease, a loan. I remember learning what a credit score was the first time I received my official green card in the U.S., and subsequently my Social Security number. I was applying for my first credit card, treating it more or less as the next step in the process of acclimating to life in the U.S. Instead, it was the opening I needed into a process that indirectly determines a huge amount of how and what you will be able to do in the country.

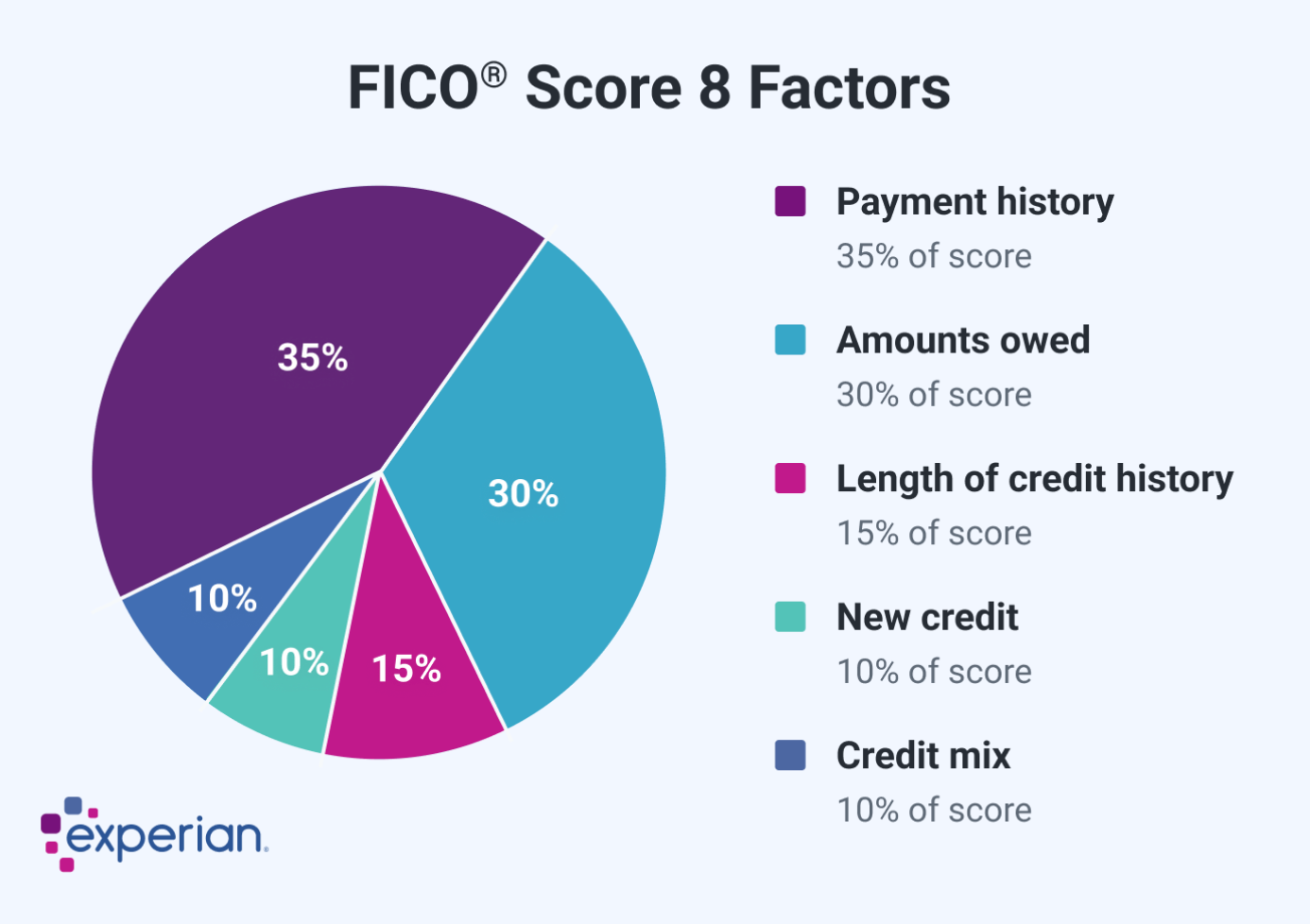

The credit score is constructed from little bits of behavioral data, late payments, credit utilization, and the age of your credit files. Each element gives an incomplete picture of who you are and what you’ve experienced in life. It is the number, however, that frequently ends up being the frame through which an entire institution views you. It starts to subtly, almost imperceptibly to you, inform how you can live, how you navigate the world, and what you think is possible in life.

This is the persuasive power of digital identity in action. Fragments of behavior are substituted for character, and the people and institutions begin to substitute the stand-in for the real thing.

2. How Credit Scores Turn Life Into Data

Credit scoring doesn’t measure what’s important, but what’s easily measured.

They never ask:

- Did a medical emergency drain your savings?

- Did reduced hours force you to fall behind?

- Did you take unpaid time to care for someone?

- Are you dealing with unstable or discriminatory labor conditions?

Rather, such systems condense complex financial realities into a clean and authoritative number. As Fourcade and Healy (2017) explain, scoring systems convert the complexity of social life into neat categories that appear objective even when they are painfully incomplete.

You begin to make decisions in life based on the importance of the score now that you know scoring well is crucial. People put off making purchases, think twice about opening new lines of credit, or prioritize the payment of bills in order to make the score go in the right direction.

Bit by bit, little by little, the algorithm becomes the quiet boss shaping your financial life, without your consent and without context.

3. How Institutions Use Your Score As A Shortcut

This shift is not only annoying. It is risky.

Your score now influences decisions across nearly every domain of modern life:

- rental housing;

- mortgage approvals;

- job applications (through background checks);

- insurance pricing;

- healthcare financing;

- student loans;

- utilities and phone services.

Rarely will these institutions take the time to consider why your score appears the way it does. The number is the complete picture in their eyes.

The digital identity begins to overshadow the lived one.

4. When a Number Starts Shaping How You See Yourself

Credit scores also do not only target institutions. They trickle inside.

Research shows that debt and credit instability have deep psychological consequences:

- Debt and financial problems are associated with lower self-esteem (Wang & Xiao, 2009).

- Unstable credit histories spawn shame and avoidance (Norvilitis, Kerns, & Maple, 2010).

- Predicted debt is associated with chronic stress and low control perceptions (Sweet et al. 2013).

Scoring systems carve out identity tracks such as high risk, responsible, or borderline. People gradually begin to inhabit those tracks (Fourcade and Healy, 2017). The classification becomes self-fulfilling.

That’s how self-fulfilling classification happens.

They start thinking:

- "I'm irresponsible."

- "I'm not the person who can buy a home."

- "I'll always be behind."

No one says these words directly. The score implies them. And once the label appears, people often internalize and absorb it into their sense of self.

5. Credit scores and predictive tools

Credit scores do not simply record the past. They gesture toward the future.

They tell lenders what you might do, which quietly determines which opportunities stay open and which ones close.

Because the score carries so much weight, people begin adjusting their behavior to match the predictions. Institutions sort individuals into categories. Individuals reshape themselves to fit the categories. The loop tightens.

This is predictive governance, a form of control in which managing classifications becomes a way of managing people. Credit scoring shows how quickly this logic becomes normal.

6. Why It Matters

Credit scores are not just numbers. They are systems that:

- gathers information on behavioral patterns;

- transforms it into judgment;

- treats that judgment as fact;

- utilizes it to distribute necessary resources;

- prompts individuals to reorganize their lives around it IT'S not "a number."

This creates a tool that sorts, predicts, and punishes, often in ways that amplify structural inequity.

A credit score will never measure your humanity or the circumstances that shaped your financial path. Yet it continues to decide the future for millions.

That alone is a reason to pay close attention. If a number can decide your future, then the least we can do is question the system that produces it. Understanding how credit scoring shapes inequality is the first step toward challenging it.

References

Fourcade, M., & Healy, K. (2017). Seeing like a credit score. Socio-Economic Review.

Fourcade, M., & Healy, K. (2013). Classification situations: Life-chances in the neoliberal era. Accounting, Organizations and Society.

Norvilitis, J. M., Chen, S., & others. (2010). Financial stress, self-efficacy, and mental health. Journal of Financial Therapy.

Sweet, E., Nandi, A., Adam, E. K., & McDade, T. (2013). The high price of debt: Household financial debt and psychological well-being. Social Science & Medicine.

Wang, J., & Xiao, J. J. (2009). Buying behavior, debt, and self-esteem. Journal of Consumer Affairs.

Fourcade, M., & Healy, K. (2013). Classification situations: Life-chances in the neoliberal era. Accounting, Organizations and Society.

Norvilitis, J. M., Chen, S., & others. (2010). Financial stress, self-efficacy, and mental health. Journal of Financial Therapy.

Sweet, E., Nandi, A., Adam, E. K., & McDade, T. (2013). The high price of debt: Household financial debt and psychological well-being. Social Science & Medicine.

Wang, J., & Xiao, J. J. (2009). Buying behavior, debt, and self-esteem. Journal of Consumer Affairs.

Sweet, E., Nandi, A., Adam, E. K., & McDade, T. W. (2013). The high price of debt: household financial debt and its impact on mental and physical health. Social science & medicine (1982), 91, 94–100. https://doi.org/10.1016/j.socscimed.2013.05.009